Picture this scenario: your traditional valuation methods might suggest a $100M valuation for an AI-native company, yet the market values it at $1B based on the most recent fundraise.

This isn’t an isolated incident – it’s a pattern we’re seeing across the AI landscape. At Stepmark Partners, the premier investment bank dedicated to the AI industry, we regularly encounter this disconnect between conventional valuation approaches and market reality.

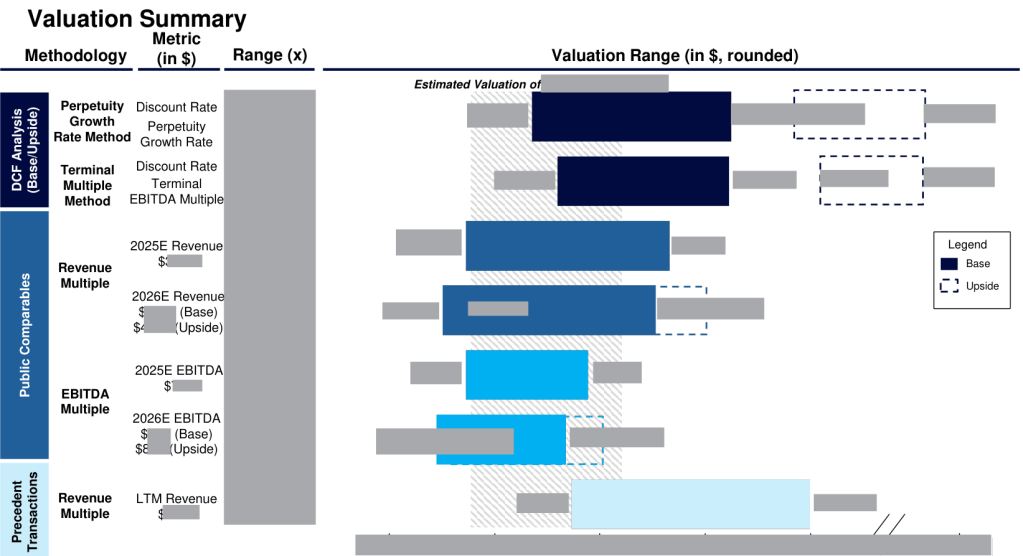

The Traditional Playbook (aka the “Football field valuation”)

Investment bankers have long relied on three primary valuation methods:

- Discounted Cash Flow (DCF) analysis

- Public comparable company analysis

- Precedent transactions

While these methods have worked well for traditional / legacy software industries, they struggle to capture the unique characteristics and potential of AI-native companies.

Why AI-native Companies Are Different

Several fundamental characteristics of AI-native companies make them particularly challenging to value using traditional methods:

1. High R&D Costs with Uncertain Payoff Timelines

Unlike your typical software companies, AI-native companies often require substantial upfront investment in research, data collection, and model development before generating revenue. Most AI startups invest millions in computing resources and talent before launching their first product. Traditional valuation models struggle to account for these irregular investment patterns and uncertain payoff timelines. From a purely modeling perspective, a DCF analysis should be projected as far as it takes to reach a steady state (e.g., 10 years or more) otherwise the volatility in business performance will making valuation difficult if the projection period is too short. Even in biotech valuation, which assumes generics come to market, it’s not uncommon to have 20 or 30 year DCF models!

2. Initial Negative Gross Margins Aren’t a Red Flag

… any assumption you make and any dollar you spend on optimizing your software will be worthless within the year. So forget it. Rely on competition in the marketplace between Claude, OpenAI and Gemini to reduce costs to a point where it doesn’t matter – Vinod Khosla (link)

Traditional valuation methods often penalize companies with negative gross margins. However, for AI-native companies, negative gross margins in the early stages shouldn’t be an immediate concern. Token prices for AI model inference have already dropped by an order of magnitude, and this trend is expected to continue. As AI models become more efficient and computing costs decrease, gross margins naturally expand. Forward-thinking investors understand that AI-native company founders should focus on product-market fit and user acquisition rather than prematurely optimizing for gross margins. This temporary trade-off between growth and margins requires a different analytical framework than traditional software companies.

3. Network Effects and Data Moats

AI companies often benefit from powerful network effects – as more users interact with their systems, the AI models improve, attracting more users. This creates a data moat that becomes increasingly valuable over time. Traditional valuation methods weren’t designed to quantify the compounding value of data assets and network effects. This is especially important as data is quickly becoming the new oil.

4. Non-linear Growth Potential

AI companies can scale rapidly once they achieve product-market fit. A single breakthrough in model performance can lead to exponential growth, making traditional growth projections based on historical data less relevant. We’ve seen numerous cases where AI companies scale from zero to significant revenue in months rather than years.

5. Limited Comparable Companies

Many AI companies are creating entirely new markets or disrupting existing ones in unprecedented ways. This makes comparable company analysis challenging – how do you value a company when there are no true public comparables? Sure, there are public companies that have AI in their name but they are a long way from being truly AI-native.

A New Framework is Needed

To properly value AI companies, we need to consider additional metrics that capture their unique characteristics:

Technical Performance Metrics:

- Model accuracy and performance metrics

- Compute efficiency and infrastructure scalability

- Data asset quality and uniqueness

- Token cost per inference

- Model optimization rates

Cost Structure and Margin Metrics:

- Gross margin trajectory over time

- Computing cost trends by model type

- Token pricing evolution

- Infrastructure cost per customer

- Cost reduction from model optimization

- Margin expansion potential at scale

Business Impact Metrics:

- Network effect strength and data moat depth

- R&D efficiency and deployment velocity

- Customer acquisition costs and retention rates specific to AI products

- Unit economics excluding temporary compute costs

- Revenue per inference

Market Position Metrics:

- Technology lead time versus competitors

- Patent portfolio strength

- AI talent acquisition and retention

- Access to compute resources

- Partnerships with cloud providers

Common Valuation Pitfalls

Traditional valuation methods often miss critical value drivers in AI companies:

- Overemphasizing current gross margins: Early-stage negative margins can mask the true potential of AI companies as compute costs decline

- Undervaluing data assets: Many AI companies possess unique datasets that grow more valuable over time

- Ignoring technical advantages: Superior model accuracy or processing efficiency can translate into lasting competitive advantages

- Missing network effects: The compound impact of AI improvements through user interaction is often overlooked

- Underestimating scaling potential: The ability to scale AI solutions globally with minimal marginal cost isn’t captured in traditional metrics

- Misunderstanding cost trajectories: Failing to account for the rapid decline in AI infrastructure and inference costs

Looking Forward

As AI continues to transform industries, the investment banking community needs to evolve its valuation approaches. The key isn’t to abandon traditional valuation methods entirely, but to augment them with new metrics that capture the unique value drivers of AI companies.

Investment bankers need to develop frameworks that combine:

- Traditional financial metrics

- AI-specific technical metrics

- Data asset evaluation

- Network effect potential

- Technical talent assessment

- Cost trajectory analysis

- Margin expansion potential

This requires a deep understanding of both AI technology and finance – a combination that lies at the heart of Stepmark Partners’ expertise as the premier investment bank dedicated to the AI industry.

Are you building an AI company and wondering about its true value? Connect with Stepmark Partners to learn how our specialized AI valuation frameworks can help you tell your company’s full story to investors and acquirers.

This article was written by the team at Stepmark Partners, the premier investment bank dedicated to the AI industry. Connect with us on LinkedIn or on X and sign up for our weekly newsletter.